Hugo Boss: The Best News is the Absence of Very Bad News

A little more than a year ago, Hugo Boss's stock collapsed amid a profit warning. 2016 has not been better, but the markets have been benevolent this time.

Indeed, poor sales in China and the US, especially in the wholesale channel caused a worrying stagnation of profits. This year the figures have been even worse: sales have fallen by 4% sales in America have not improved and earnings per share have gone from EUR 4.63 in 2015 to 2.80 in 2016 and although there is no expectations that in 2017 the company will grow, at least there is a consensus that the German company has touched ground, which has made important and adequate adjustments as the closing of the most deficient stores as well as a repositioning of Hugo, his least exclusive brand to pass it sector Premium to a category, lets say, more democratic.

On the other hand, the company’s online strategy especially in China is paying off, the brand is able to reach an increasing number of unique followers in social networks at the same time it has improved by 20% in 4th quarter.

Laying the foundation for sustainable growth … from 2018

The company announced the results of the group’s results for the full year 2016. For the year, the company announced that as part of the action plan, it accepted sales losses linked to reductions in points of sales and support to retailers. EBITDA before special items fell by 17%, reflecting a decline that would have been even greater if the company had not taken effective measures to reduce certain costs. However, cash flow increased, underscoring a better focus on the investment activity of the particular group.

Starting with the top line, full-year sales grew by 1% in Europe. In the United Kingdom continued to grow solidly, specifically 8% in the year, driven by the announcement of Brexit. Sales in Germany and France fell by 4% and 3%, respectively. In the Americas, full year sales in local currencies were 12% lower than in the previous year. This was mainly due to the US, where sales were reduced by 17%. In North America precisely, the company registered a decrease of almost 30%, in the wholesale business.

The special items we have indicated amounted to EUR 67 million, which correspond mainly to payments of termination of rental contracts and other reductions in relation to closures of stores already planned. Net profit fell sharply to EUR 194 million. The core of the 2017 strategy is to focus the portfolio on two brands of BOSS and HUGO. Various discussions with final customers and wholesale partners revealed that the positioning of their brands was not clear and understandable enough.

Therefore, the company decided to integrate the brand BOSS Green and BOSS Orange into the BOSS brand. In the future, BOSS will focus on a very defined type of customer who can offer you suits for all the occasions you need: business, casual and sport. BOSS will strengthen the core of the premium brand, while the HUGO brand will focus, as we have seen HUGO in a medium segment with great growth potential.

Depending on sales performance in the retail trade itself, EBITDA before special items is also expected to move in the range of less than 3% to more 3%. This forecast assumes a steady increase in operating expenses in relation to the company’s transition to a strictly customer-oriented business model, including a slight increase in marketing expenses in proportion to sales.

The investment will remain at levels similar to those observed in 2016, and will fluctuate around EUR 160 million. About two-thirds of that budget will go to store renovation and new openings, the rest will focus mainly on new technologies, where the company will continue to improve the infrastructure needed for its digital activities. The company relies on a generation of free cash flow online at the level of the previous year. The prospects, perhaps excessively optimistic, of the company are to acquire a solid growth from 2018.

An improvable balance

The company’s current capital remained at levels around EUR 450 million , marking a current ratio of 1.63 lower than 2015 (1.76). The acid test (liquidity ratio excluding inventories) worsened from 0.80 (2015) times to 0.75 in 2016 due to an always undesirable excess of inventories.

- The percentage of equity/ total assets is under 50% in 2016 (53% in 2015).

- The number of times interest can be paid by profits have doubled since net interest payments have fallen from € 5.9 million to 2.1, which is very positive.

- The turnover of assets goes from 1.56 times in 2015 to 1.49 in 2016, which reflects worse efficiency in the use of these assets.

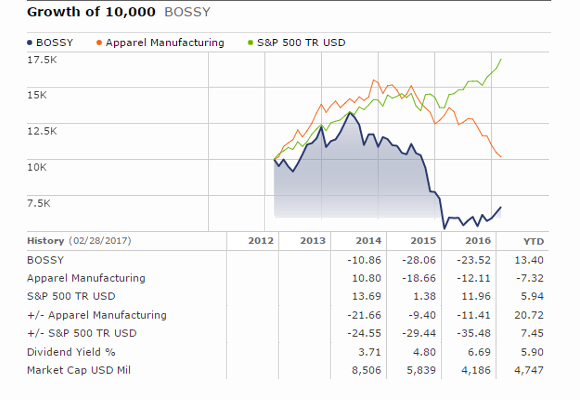

Hugo Boss AG announced a definitive dividend of EUR 2.60 per share for the 2016 fiscal year. The date of payment of said dividend is May 29, 2017. The dividend, which has also fallen from EUR 3.62 paid in 2015, seems to give little comfort to a company with sad financial statements in a sector far from its best moment as it is indicated the comparison of Morningstar stock indexes.

Disclosure: The Luxonomist is not responsible for the views expressed in the article. The text has been written freely expressing their own ideas, without receiving any compensation. The author has no business relationship with any of the companies whose shares are listed in this article.