Eurodeal-Luxonomist index: Weekly evolution

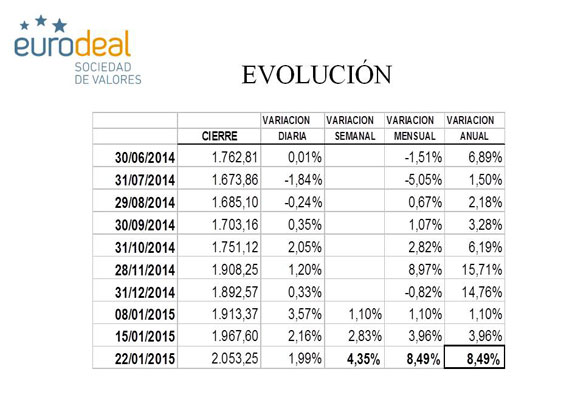

Our index has behaved spectacularly, with a rise in the week of the 4.35% to position in the month and the year in a 8.49%

Weekly inform number 30. What a week!!! Five days, practically, of rise in the stock market, marked by Friday´s closing, really positive after the BCS announcement of abandonment of the minimum exchange rate against the euro. On Monday, with the American market closed, the rumors about the BCS performances and the global growth forecasts, giving China a stick and improving the growth expectations for Spain, marked the markets tendency.

The uptrend increased on Tuesday with the publication of the ZEW index reliable in the German economy, while the oil price still falling. Wednesday, we learned data about housing in EE.UU (the good data of residential building in December was offset by a terrible new permits) and in the BoE transactions, we knew that two counselors of the FED that waged on a interest rate increase in USA, retracted in face of the low inflation rates risk (ten four!!) .Last Moodys published that, in the Spanish banks, the mulberry had “touched highs”.

And last, on Thursday, end of our analysis week and the D day of the European Central Bank. I have to recognize that Don Mario has surprised me. I won’t go into if QE measures will be a balm for European economy or not (hopefully!), but the measures involvement has exceeded my expectations. In my article that was published on Thursday in this medium, predicted:

“This measures are summarized in applying, according to forecasts, 550 billion Euros (50 billion monthly until December 2015)”, It has been more, 60.000 million Euros per month until September 2016, starting in March this year, but including the existing purchase private assets programs (13.000 million Euros per month). Here, the theory. But let’s be attentive to the small print. Ergo:

- “Will be the acquisition in sovereign votes or other debt? Because I fear it will only be in sovereign votes”. Well no fear, Miguel Angel, the asset purchases will affect public and private emissions.

- “Will the BCE buy the bonds or will be each central bank who buy his country bonds? Well unfortunately, I think that each central bank will assume his country risk. And this doesn´t help the “unionists chants”, or, of course, to the Greek pre-election environment. Another mistake on my part: the program seeks to pool the risks what implies that the 20% will be subject to loss-share scheme.

- “And following with Greece, Will the threat of Greek bank be fulfilled, if Troikas´s requirements aren´t executed, they won´t have access to the BCE financing? I don´t think they are able to challenge this pulse to the Hellenistic authorities”. Don Mario has made clear that discards Greek if a Troika´s program isn´t guaranteed.

Regarding to injections of cheap credit long term running (TLTRO), has been decided to change the price of the six pending auctions, removing the differential 10 basis points that were being implemented to the first TLTRO, maintaining the interests rates in the 0,05%. Measures, the less, brave and silencing the voices that predicted the German influence, will decaffeinate the background and the form thereof.

Thus, in this context, the Ibex raised in the week in a 5,29%, the Dow Jones a 2,22%, while the Eurostoxx 50 managed to finish the week with rises of the 5,24%. Regarding the currency, the Dollar continues to strengthen against the Euro, and took a 9%, (1.1383) and the Brent in its downward climbing, with strong volatility (48, 52$/barrel).The Spanish 10-year bond closed in 1.405% (historic minimums) and the risk premium in 95,7 (lowest level since 2010).

Our index, as usual, and long, in the last months, has behaved spectacularly, with a rise in the week of the 4.35% to position in the month and the year in a 8.49%, thanks, above all, the strengthening of the Dollar on the Euro.

The five values that better behaved this week were:

- KATE SPADE 8,67%

- TIFFANY 8,60%

- SALVATORE FER 8,47%

- COACH 7,92%

- BMW 7,65%

Conversely, the five values that behaved worse in the week were:

- SWATCH -7,00%

- RICHEMONT -2,45%

- HERMES -1,35%

- PRADA 0,74%

- LVMH 2,07%

See the technical analysis of the Index:

As we indicated last week, after the break of the level 1947, we have no choice, but to wait new maximums in our index, which has occurred. The trend indicators are positive although the relative strength don´t accompany this tendency, so we don´t rule out some consolidation in this levels. As to Ichimoku, the positive cloud start a narrowing, supports this idea. As we can see, the top of the cloud is being support to the index prices. In brief, we maintain our bullish outlook, while, we don´t rule consolidate this short-term levels.

“The strength of the brave, when they fall, is passed to the weakness of those who rise”, Miguel de Cervantes.

Analysis: Miguel Angel Abad Chamon, Minister of Eurodeal Sociedad de Valores,AbadMaachamon

Disclosure: This report is provided for information purposes. The opinions contained in it are based on information obtained from sources believed to solvents but we can not guarantee its accuracy and correctness. Our opinions are discharged at a given time and are subject to change over time. Eurodeal not accept any liability for losses to follow the recommendations expressed in this report.