In Bernard Arnault words, LVMH´s president and CEO (Chief Operate Officer): “The 2014 results, confirm the LVMH capacity to continue progressing in spite of the economic and currency uncertainty. We have reached a record income and net profit”. Mr. Bernard has us accustomed to this grandiloquent comments, but lack of the necessary depth, after analyzing the group annual accounts. And that is what I pretend to do in this article, with the intention of not overwhelm the suffering readers, with a data battery, without explaining the endogenous or exogenous reasons that have affected to the Company´s evolution.

Sales amounted to 30.638 million euros, what supposes a annual growth of the 5,59%. France and Asia were below the expectations, while United Estates, significantly increased the Group sales.

By products:

The gross profit grew in a 4,30%, burdened by the cost of sales increase (+8,04%). For this reason the Gross margin fell in 80 p.b. during 2014. (not so record, Mr. Bernard). The operating profit amounted € 5.431 millions, face of the € 5.898 millions of last year. This represents a fall of the -7,92%. The expenses of merchandising and sales (+9,07%) and the general expenses and administrative (7,28%), were responsible of this fall. The operative margin stood in a 17,73%, with a fall of 260 p.b.

By products:

The net profit attributed to the Group, thanks to a financial net result of € 2.947 millions, grew on a 64,38%,with a amount of € 5.648 millions. The net margin stood in a 18,43%, with a grown of 659 p.b. Specifically, the epigraph “Other financial incomes and expenses”, collect in benefits of € 3.189 recognized millions after the exceptional distribution in specie of the Herme´s actions.

The perspectives of the Company for the year that has initiated are to keep pace of the sale´s growing, although the otherwise economic climate, currency tensions and the geopolitical uncertainties. Further, the Company, has announced a dividend increase of the 3%. In the ordinary general meeting of shareholders of the 16 of April of 2015, will propose a dividend of 3,20 € per share. As well, we are going to analyze the results of the Balance and of the income statements: In regard to the evolution of the indebtedness, the Company maintains more than a proper balance between the own and other funding:

According to the short term solvency:

Other positive point is the increase of the Working Capital in more than a 37% about last year.

Regarding to the Sale analysis:

As I have already indicated, with a deceleration in the Chinese growth, the geopolitical problems, and the Exchange rate fluctuations, improve in more than a 185 p.b. the sales increase , with respect to the period 2012-2013,it´s a success. Everyone seems to expect double-digit growths, but with a very low inflation of the most advanced economies, this growth of the 5,59% is seen amplified.

Even if , the Company should review his expenditure program, inasmuch as a cost of sale increase in a 8,04%, of Marketing and Sales in a 9,07% and General and Administrative in a 7,28% (all of them above the increase in sale percentage) are not supportable in the result´s account, except for atypical.

So, the Profitability of the own funds, thanks to the Financial incomes has been spectacular, doubling. Even if, the Actives profitability has fallen in more than a 30 p.b. In brief, the Company´s results are biased by the appearence of atypical benefits.For 2015 present certain uncertainties outside the Company that, the less, are going to hinder the growth rhythm maintenance.

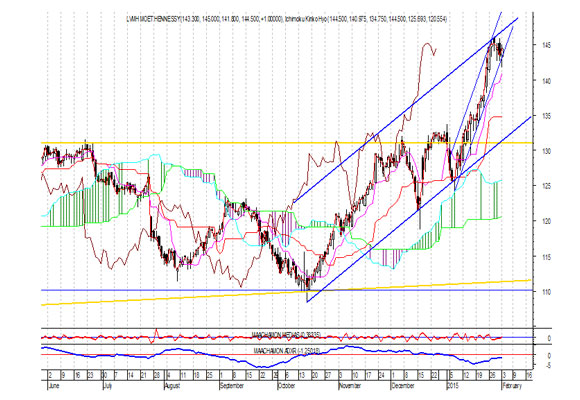

Technical analysis of the Value

If we look the weekly graphic:

We can see that the value is located in the top of a bullish subchannel. Once broken the resistance in 131,10 four weeks ago, the value´s target Price is of 155,90. The trend indicators are positive, although the Relative Strength indicators give slight signs of exhaustion. In regard to Ichimoku, the narrowing of the bands can support the end, short term of this movement.

If we analyze the diary graphic, is confirmed what we saw in the weekly. The trend indicators are bullish, but the Relative Strength indicators advise us to be out of the value.

In brief, we like the long term value, with objective 155,90 €/action, while a short term, we don´t discard cessions (not further of the 137.70),that should be exploited for the short positions taking of the value. «If I doubt, if I hallucinate, I live. If I fool myself, I exist. How to fool myself stating that I exist, if I have to exist to fool me?», San Agustín.

Analist: Miguel Angel Abad Chamon. Consejero de Eurodeal, S.V.

Disclosure: This report is provided for information purposes. The opinions contained in it are based on information obtained from sources believed to solvents but we can not guarantee its accuracy and correctness. Our opinions are discharged at a given time and are subject to change over time. Eurodeal not accept any liability for losses to follow the recommendations expressed in this report.

No se puede separar la cultura de las personas, así como no se puede separar… Read More

Apenas quedan unos días para que se celebre la esperadísima Gala MET. Prácticamente todo el… Read More

Con el Día de la Madre a la vuelta de la esquina son muchos los… Read More

Hacía tiempo que los relojes orientales provenientes de una colección privada no llegaban al mercado.… Read More

Los aficionados a la música son exigentes eligiendo qué dispositivo les lleva el sonido hasta… Read More

El acento puede ser una gran catalizador cuando estamos conociendo a alguien. No solo qué… Read More

Este sitio utiliza cookies para prestar sus servicios y analizar su tráfico. Las cookies utilizadas para el funcionamiento esencial de este sitio ya se han establecido.

{kind=link}

{kind=link}